Aequs Limited

The Structural Integrator of Global Aerospace Supply Chains

Table of Contents

1. Executive Summary: The Strategic Imperative of Vertical Integration

Structural Positioning and “China Plus One”

The “One-Stop-Shop” Model and Vertical Integration Moat

Financial Context: The Deleveraging Catalyst of the IPO

2. Investment Thesis and IPO Structure Analysis

2.1 The Offering Dynamics

Issue Size, Structure, and Valuation

2.2 Capital Allocation: The Deleveraging Narrative

Repayment of Outstanding Borrowings and Interest Reduction

Impact on EPS and Working Capital Resilience

Planned Capital Expenditure (Capex)

3. Corporate Genesis: The Engineering DNA

Founder’s Background and QuEST Global Lineage

Transition from “Build-to-Print” to “Ecosystem” Model

The Cluster Philosophy: Belagavi, Koppal, and Hubballi Clusters

4. The Aerospace Segment: A Deep Dive into the Core

4.1 The “One-Stop-Shop” Capability Spectrum (Vertical Integration)

4.1.1 Forging: The Foundation (SQuAD Forging India JV)

10,000-ton hydraulic press capability

4.1.2 Precision Machining: The Core Competency

3, 4, and 5-axis CNC technology and hard-metal expertise

4.1.3 Surface Treatment: The Bottleneck Breaker (Aerospace Processing India - API JV)

Nadcap and OEM Approvals (Airbus, Boeing)

4.1.4 Structural Assembly

4.2 Product Portfolio Analysis (4,500+ SKUs)

4.3 Client Ecosystem and Program Exposure

Key Clients (Airbus, Boeing, Safran, etc.)

Exposure to A320neo, 737 MAX, and Widebody Programs

5. Barriers to Entry: The Fortress of Aerospace

5.1 The Certification Gauntlet

AS9100 Rev D and Nadcap Accreditations

Customer Approvals (Approved Supplier List)

5.2 The “First Article Inspection” (FAI) Moat

AS9102 Process and “Frozen Process”

High Switching Costs for OEMs

5.3 Capital Intensity and Gestation Timeline

6. Diversification Strategy: Beyond Aerospace

6.1 The Koppal Toy Cluster (KTC): The China+1 Play

Strategic Rationale and Key Clients (Hasbro, Mattel)

Shift to Original Design Manufacturer (ODM) role for Disney

6.2 Consumer Durables & Electronics: The Apple Connection

Hubballi Durable Goods Cluster (HDC)

Synergy with Aerospace Machining Expertise (MacBook/Watch Enclosures)

7. Financial Analysis and Peer Benchmarking

7.1 Deconstructing the Financials

Revenue, EBITDA, and Net Loss Analysis

The Financial Pivot: Impact of Debt Repayment on Profitability

7.2 Peer Comparison

Valuation Metrics (P/S) vs. Azad and PTC

Argument for Undervaluation based on Asset Base and Scale

8. Risk Factors

Titanium Supply Chain Volatility (Russian Exposure)

Customer Concentration (Airbus and Boeing Production Rates)

Execution Risk in Low-Margin Consumer Segment

Currency Fluctuation Risk (Forex)

9. Conclusion

Final Assessment: Infrastructure Play on Global Aerospace

Long-Term Outlook and Investment Horizon

1. Executive Summary: The Strategic Imperative of Vertical Integration

The forthcoming Initial Public Offering (IPO) of Aequs Limited marks a watershed moment for the Indian precision manufacturing sector, presenting institutional and retail investors with a rare vehicle to access the high-entry-barrier global aerospace supply chain. As the geopolitical tectonic plates of manufacturing shift away from single-source dependency on China, Aequs has emerged not merely as a beneficiary of this “China Plus One” strategy, but as a sophisticated architect of a vertically integrated ecosystem that major global Original Equipment Manufacturers (OEMs) like Airbus and Boeing desperately require.

This comprehensive research report initiates coverage on Aequs Limited with a constructive long-term outlook, predicated on the company’s unique structural positioning. Unlike traditional contract manufacturers that operate as fragmented nodes in a supply chain, Aequs has successfully operationalized a “one-stop-shop” model within India’s first notified precision engineering Special Economic Zone (SEZ) in Belagavi. This ecosystem integrates the entire value chain—from metallurgical forging and precision machining to special processing (surface treatment) and final assembly under a single customs and logistical umbrella. This integration is a formidable defensive moat, creating sticky, multi-decade relationships with clients who face immense switching costs.

While the headline financial metrics for FY2025 indicate a net loss of ₹102.3 crore , our deep-dive analysis suggests this is a lagging indicator of a heavy capital expenditure cycle rather than a reflection of operational fragility. The company is currently burdened by finance costs associated with the debt raised to build this world-class infrastructure. The IPO, structured primarily to retire ₹433.17 crore of this debt , acts as a critical deleveraging catalyst that is expected to unlock the company’s latent profitability. By removing the interest burden, Aequs is positioned to transition from a capital-hungry growth engine to a free-cash-flow generating industrial compounder.

Furthermore, the company’s strategic diversification into consumer verticals—specifically the Koppal Toy Cluster and the burgeoning relationship with consumer electronics giants (reportedly including Apple)—provides a hedge against the inherent cyclicality of the aerospace sector. This report dissects the granular details of Aequs’ operations, the insurmountable barriers to entry that protect its market share, and the financial inflection point that this IPO represents.

2. Investment Thesis and IPO Structure Analysis

2.1 The Offering Dynamics

Aequs Limited is entering the public markets with a total issue size of approximately ₹921.81 crore, comprising a fresh capital injection of ₹670 crore and an Offer for Sale (OFS) of ₹251.81 crore by existing shareholders and promoters. The price band of ₹118–₹124 implies a post-money market capitalization exceeding ₹8,300 crore.

2.2 Capital Allocation: The Deleveraging Narrative

The utilization of the fresh issue proceeds is the single most important variable in the investment case for Aequs. The company has explicitly earmarked ₹433.17 crore—nearly 65% of the fresh issue—for the repayment or prepayment of outstanding borrowings.

This allocation is strategic rather than defensive. The aerospace industry is characterized by a “J-curve” investment profile: immense upfront capital is required to build facilities, install high-tonnage presses, and secure qualifications (a process taking 3-5 years) before a single dollar of revenue is realized. Aequs has historically funded this gestation period through debt. Now that the capabilities are established and the order book is mature, retiring this debt serves two critical functions:

EPS Accretion: The reduction in interest expense will flow directly to the bottom line. In FY25, finance costs were the primary driver of the reported net loss. Post-IPO, the interest coverage ratio is expected to improve dramatically, instantly making the P&L look healthier.

Working Capital Resilience: Aerospace manufacturing is working-capital intensive due to the high cost of raw materials (titanium, Inconel) and long production cycles (inventory days stood at 253 in FY25). A cleaner balance sheet allows Aequs to negotiate better terms with lenders for working capital facilities, further reducing the cost of capital.

Additionally, ₹64 crore is allocated for capex to purchase new machinery , signaling that demand is outstripping current capacity in specific high-value segments.

3. Corporate Genesis: The Engineering DNA

To understand Aequs, one must understand its lineage. The company was founded by Aravind Melligeri, a mechanical engineer and co-founder of QuEST Global, one of the world’s leading engineering services firms. This background is pivotal. Unlike a traditional manufacturing promoter who starts with a machine shop, Melligeri started with engineering design.

QuEST Global’s deep relationships with the R&D and engineering divisions of Airbus, Boeing, and GE gave Aequs (formerly QuEST Global Manufacturing) an unparalleled “right to win.” The company understood the design intent behind the parts, not just the manufacturing drawings.

In 2014, the manufacturing business was spun off as Aequs to create a distinct identity focused on physical asset creation. Melligeri’s vision was to move beyond the “build-to-print” model (where a supplier simply follows a drawing) to an “ecosystem” model. He recognized that the biggest pain point for global OEMs was not the cost of machining, but the logistical nightmare of managing a fragmented supply chain where a part moves between five different suppliers for forging, machining, treatment, and testing.

Aequs was built to solve this logistical inefficiency. The company’s philosophy is anchored in creating clusters:

Belagavi Aerospace Cluster (BAC): The flagship aerospace ecosystem.

Koppal Toy Cluster (KTC): A labor-intensive manufacturing hub.

Hubballi Durable Goods Cluster (HDC): A consumer electronics and appliances hub.

This cluster approach allows Aequs to share infrastructure costs (power, water, security, logistics) across multiple units, driving operational leverage that standalone factories cannot match.

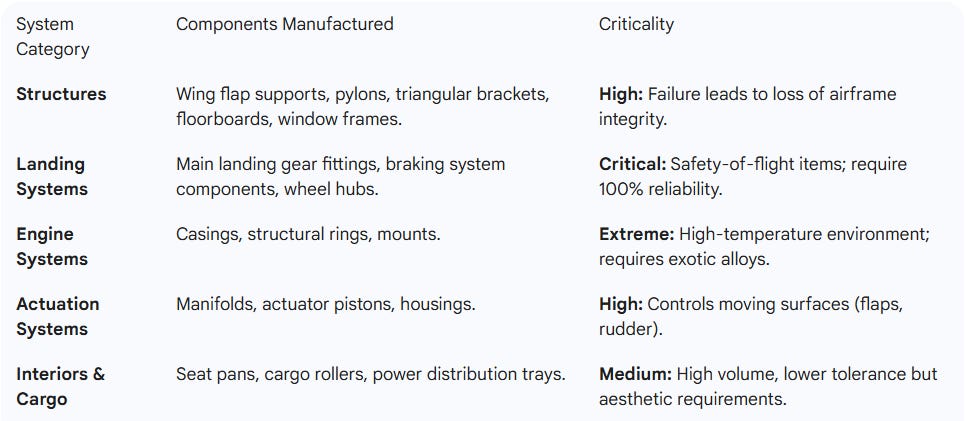

4. The Aerospace Segment: A Deep Dive into the Core

The Aerospace segment is the financial and strategic engine of Aequs, contributing approximately 90% of revenue in FY25. Aequs is not a commodity player; it is a critical node in the safety-critical supply chain of commercial aviation.

4.1 The “One-Stop-Shop” Capability Spectrum

Aequs distinguishes itself through Vertical Integration. In the context of aerospace, this means controlling every step of the transformation of metal into a flight-ready component. This integration is achieved through a mix of wholly-owned units and strategic Joint Ventures (JVs) located within the Belagavi SEZ.

4.1.1 Forging: The Foundation (SQuAD Forging India)

The manufacturing process begins with forging—shaping metal using extreme pressure to align its grain structure for maximum strength. This is critical for parts like landing gear and engine mounts that bear immense loads.

The Joint Venture: Aequs partnered with Aubert & Duval, a French metallurgical specialist and a world leader in high-performance alloys, to form SQuAD Forging India Pvt Ltd.

Capabilities: The facility houses a 10,000-ton hydraulic press, one of the largest in the private sector in India. This press allows SQuAD to forge large, complex structural components and landing gear parts that smaller presses cannot handle.

Significance: Most competitors must import forgings or buy them from external vendors, adding weeks to lead times and layering margins. SQuAD allows Aequs to control the raw material input.

Track Record: SQuAD recently celebrated the production of its 25,000th aircraft wheel, a testament to its volume capabilities and certification maturity.

4.1.2 Precision Machining: The Core Competency

Once forged, the metal “blank” must be machined to micron-level tolerances.

Technology: Aequs operates a massive fleet of 3, 4, and 5-axis CNC (Computer Numerical Control) machining centers. 5-axis machining is essential for aerospace parts which often have complex, organic curves (aerodynamic shapes) that cannot be machined with standard 3-axis tools.

Materials: The company specializes in hard-metal machining, working with Titanium, Inconel, and aerospace-grade steel. These materials are notoriously difficult to cut; they generate immense heat and wear out tools rapidly. Aequs’ expertise in “speeds and feeds” for these exotic alloys is a significant technical barrier.

Capacity: The company has installed capacity of over 2.9 million machining hours annually.

4.1.3 Surface Treatment: The Bottleneck Breaker (Aerospace Processing India - API)

After machining, aerospace parts must undergo “Special Processes” to protect them from the extreme environment of high-altitude flight (corrosion, wear, fatigue). This is often the chokepoint in the global supply chain because these processes involve hazardous chemicals and require strict environmental clearances.

The Joint Venture: Aequs partnered with Magellan Aerospace (Canada) to form Aerospace Processing India (API).

Capabilities: API provides anodizing, cadmium plating, passivation, painting, and Non-Destructive Testing (NDT).

Strategic Moat: Establishing a surface treatment plant in India is incredibly difficult due to pollution control board regulations regarding Zero Liquid Discharge (ZLD). Aequs has already solved this. API was the first third-party facility in India approved by both Airbus and Boeing , meaning Aequs does not need to ship parts to Europe or the US for finishing.

Expansion: Aequs and Magellan are currently exploring expanding this partnership to include Engine MRO and Sand Casting, further widening the capability gap against peers.

4.1.4 Structural Assembly

The final step is assembling individual components into sub-assemblies (e.g., a wing flap mechanism). Aequs performs this integration, delivering “plug-and-play” units to the customer’s final assembly line. This captures more value than selling loose parts.

4.2 Product Portfolio Analysis

Aequs manufactures over 4,500 unique parts (SKUs). This diversity shields the company from the obsolescence of any single part.

4.3 Client Ecosystem and Program Exposure

Aequs has achieved “Approved Supplier” status with the duopoly that controls global aviation. This is a binary outcome you are either on the list or you are not. Aequs is firmly on it.

Key Clients: Airbus, Boeing, Safran, Collins Aerospace, Spirit AeroSystems, Eaton, Honeywell, Saab, Bombardier.

Program Exposure:

Airbus A320 Family: The workhorse of global aviation. Aequs supplies parts for the A320neo, benefiting from the massive backlog of over 6,000 aircraft.

Boeing 737 MAX: Despite recent production caps, this remains a high-volume program. Aequs manufactures landing gear components for it.

Widebodies: A350, A330, B777, B787. These high-value programs use more titanium and large forgings, playing to SQuAD’s strengths.

5. Barriers to Entry: The Fortress of Aerospace

Investors often ask: “Why can’t a general engineering firm enter this market?” The answer lies in the formidable barriers to entry that Aequs has surmounted over the last 15 years.

5.1 The Certification Gauntlet

Entering aerospace is a regulatory odyssey.

AS9100 Rev D: This is the baseline Quality Management System. It is far more stringent than ISO 9001, requiring rigorous configuration management and traceability.

Nadcap (National Aerospace and Defense Contractors Accreditation Program): This is the gold standard for special processes. A Nadcap audit is invasive; auditors check everything from the calibration of the oven to the chemical composition of the plating bath. Failure leads to immediate suspension. Aequs holds Nadcap accreditations for Forging, Heat Treatment, NDT, and Chemical Processing.

Customer Approvals (The “Approved Supplier List”): Even with AS9100 and Nadcap, a supplier cannot make a Boeing part without Boeing’s specific approval (e.g., D1-4426). Gaining this approval takes years of audits.

5.2 The “First Article Inspection” (FAI) Moat

The AS9102 First Article Inspection is the single biggest operational barrier.

The Concept: Before mass production, a supplier must produce a “First Article.” Every single dimension (there can be hundreds on a complex part), every note on the drawing, and every material cert must be verified and documented.

The Cost: Performing an FAI consumes immense engineering hours and machine time, for which the supplier is often not paid. It is an upfront investment.

The “Frozen Process”: Once the FAI is approved by the OEM, the manufacturing process is “frozen.” The supplier cannot change the CNC program, the cutting tool brand, or the coolant concentration without re-qualifying.

The Switching Cost: Because qualifying a new supplier requires the OEM to pay for and oversee a new FAI process (which is risky and expensive), OEMs are incredibly reluctant to switch suppliers once a part is in production. This gives Aequs massive incumbency advantage.

5.3 Capital Intensity and Gestation

The aerospace business model requires a “leap of faith.” A supplier must invest in high-end 5-axis machines (costing $500k - $1M each) and infrastructure before receiving a single contract.

The Timeline: It takes ~18-24 months to build a plant and get basic certs. It takes another 12-24 months to get customer approvals and pass FAIs. This means a 3-5 year period of cash burn before revenue stabilizes.

Aequs’ Advantage: Aequs has already paid this “time tax.” A new entrant starting today would be five years behind.

6. Diversification Strategy: Beyond Aerospace

Recognizing the cyclical risks of aerospace (pandemic downturns, production halts), Aequs has strategically diversified into consumer segments.

6.1 The Koppal Toy Cluster (KTC): The China+1 Play

Aequs has operationalized a 400-acre toy manufacturing ecosystem in Koppal, Karnataka.

Strategic Rationale: The global toy market is $90 billion, heavily dominated by China. As global brands like Hasbro and Mattel de-risk, India is the logical alternative due to low labor costs.

Clients: Aequs manufactures for Hasbro, Spin Master, and Disney.

Value Chain Climb: In a significant move, Aequs recently signed a deal to be an ODM (Original Design Manufacturer) for Disney. Instead of just making a toy to a drawing, Aequs designed and manufactured 36 collectible Marvel pullback cars. This shifts Aequs from a labor-arbitrage player to a value-added partner, commanding higher margins.

6.2 Consumer Durables & Electronics: The Apple Connection

The Hubballi Durable Goods Cluster (HDC) focuses on appliances and electronics.

Clients: Aequs manufactures cookware for Tramontina (Brazil) and Wonderchef.

The Apple Opportunity: Reliable industry reports indicate Aequs is in the “trial phase” for manufacturing mechanical enclosures for Apple MacBooks and Apple Watches.

Synergy: The machining of a MacBook’s unibody aluminum chassis requires the same 5-axis CNC expertise and anodizing capabilities used in aerospace. Aequs is repurposing its core competency for high-volume electronics.

Potential: If Aequs secures a spot as a mass-production supplier for Apple (joining Tata Electronics), this segment could dwarf the aerospace revenue in volume terms, though at lower margins.

7. Financial Analysis and Peer Benchmarking

7.1 Deconstructing the Financials

Investors must look past the headline loss.

Revenue: ₹925 crore in FY25 (Aerospace ~₹824 Cr).

EBITDA: Positive at ₹107.97 crore (11.68% margin). The margin compression from ~15% in FY24 is attributed to the ramp-up costs in the consumer segment and under-utilization of new capacity.

Net Loss: ₹102.3 crore. This is driven by Finance Costs and Depreciation.

The Pivot: The IPO proceeds of ₹433 crore for debt repayment will drastically reduce the interest burden. Assuming a 10% cost of debt, this saves ~₹43 crore annually, instantly bridging nearly half the gap to profitability. Combined with operational leverage from higher capacity utilization, Aequs is poised for a turnaround.

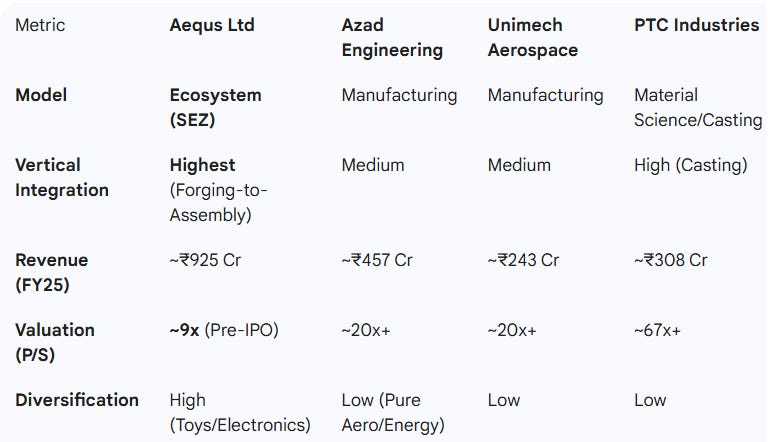

7.2 Peer Comparison

Aequs is unique, but comparisons help frame the valuation.

Analysis: Aequs trades at a discount (Price-to-Sales) relative to peers like Azad and PTC. This discount exists because Aequs is currently loss-making while peers are profitable. However, Aequs has a significantly larger revenue base and a more integrated asset base. If the management executes the deleveraging and operational efficiency plan, the valuation gap represents a significant upside opportunity for investors.

8. Risk Factors

Titanium Supply Chain: The aerospace industry relies on Russian titanium. While Aequs states supply constraints are “nearing resolution” , global price volatility remains a risk to margins.

Customer Concentration: Aequs is dependent on the production rates of Airbus and Boeing. Any production halt (e.g., a strike at Boeing or a grounding of a specific aircraft type) ripples down immediately to Aequs.

Consumer Segment Execution: The consumer electronics business is high-volume but low-margin and unforgiving. A failure to meet yield targets could result in heavy losses, as seen with other contract manufacturers entering this space.

Currency Fluctuation: With ~90% of revenue from exports (USD/EUR) and significant debt/capex potentially in foreign currency, forex volatility is a constant variable.

9. Conclusion

Aequs Limited is not a standard manufacturing play; it is an infrastructure play on the global aerospace supply chain. The company has built a moat of vertical integration, regulatory certification, and customer trust that is structurally difficult to replicate.

The IPO offers investors a chance to enter at the bottom of the profitability curve. The capital raised will repair the balance sheet, allowing the underlying quality of the aerospace business to shine through. While risks regarding execution and cyclicality persist, the structural tailwinds of the “China Plus One” strategy and the robust order backlogs of global OEMs position Aequs as a compelling long-term compounder in the Indian industrial landscape. For investors with a 3-5 year horizon, Aequs offers a strategic entry point into the high-value manufacturing renaissance of India.

Disclaimer: This is not a buy or sell recommendation. I’m not a SEBI-registered investment advisor, and nothing shared here should be taken as financial advice. This content is purely for educational and informational purposes. I’m not affiliated with SEBI or any brokerage, nor am I trying to promote or sell anything. Always do your own research before making any investment decisions.